Key Highlights

- You have a strict clock: send the demand notice within 30 days of the bank's return memo, then file the complaint within 30 days after the drawer's 15-day payment window ends.

- The cheque must be presented within 3 months of its date — an old cheque can't anchor a Section 138 case.

- You file where YOUR bank branch is — not where the person who gave you the cheque lives.

- Under Section 143A, the court can order the drawer to pay you up to 20% of the cheque amount as interim compensation while the case is still running.

- Section 138 carries up to 2 years' jail or a fine up to twice the cheque amount — but the realistic outcome is compensation, not custody.

- A conviction is not the same as getting your money. Plan for recovery from day one.

- Missing the 30-day notice deadline usually kills the case before it starts.

Someone gave you a cheque. It bounced. You're holding a return memo from the bank and a quiet, specific kind of anger — because this wasn't a misunderstanding, it was a payment that didn't happen.

Take Meera, who runs a small interior-design studio in Pune. A contractor owed her ₹3,00,000 for finished work and paid by cheque. She deposited it; three days later it came back stamped "funds insufficient." Now what?

The short version, up front: present the cheque within 3 months, send a written demand notice within 30 days of the bounce, give the drawer 15 days to pay, then file your complaint in the next 30 days — in the court where your own bank branch sits. Miss a window and the case can collapse.

That's the spine of how you file a cheque bounce case under Section 138 of the Negotiable Instruments Act, 1881 (the law that makes cheque dishonour a punishable offence in India). Now the detail, step by step — with Meera's ₹3 lakh cheque as the running example.

First, Is This Even a Section 138 Case?

Before anything else, check that your situation fits. Not every bounced cheque becomes a criminal case. You need all of these to be true:

The cheque was issued to you for a legally enforceable debt or liability — payment for goods, services, a loan repayment. Meera's cheque was for completed work, so she's fine. A gift cheque or a donation is not.

It bounced for a reason the law recognises — usually "insufficient funds," but "account closed" and "payment stopped" count too.

You presented it within its validity period (more on this below).

If the cheque was handed over as a blank security cheque, or there was no real debt behind it, the case gets harder — that's the ground the drawer will fight on later. If that's your situation, read our piece on cheque bounce defence strategies first, so you know what the other side will argue.

Step 1: Present the Cheque Within 3 Months

A cheque in India is valid for three months from the date written on it (the RBI cut this from six months back in 2012). Deposit it after that and the bank won't honour it — and a cheque that was never validly presented can't anchor a Section 138 case.

So bank it within a week or two, like Meera did. If it bounces, you can re-present it within those three months — and the Hon'ble Supreme Court in MSR Leathers v. S. Palaniappan (2013) 1 SCC 177 confirmed that a fresh cause of action can arise on a later dishonour. Useful, but don't lean on it. Treat the first bounce as your trigger.

So what does this mean for you? Don't sit on a cheque. The validity window is the first deadline, and it's the easiest one to lose by accident.

Step 2: Get the Cheque Return Memo

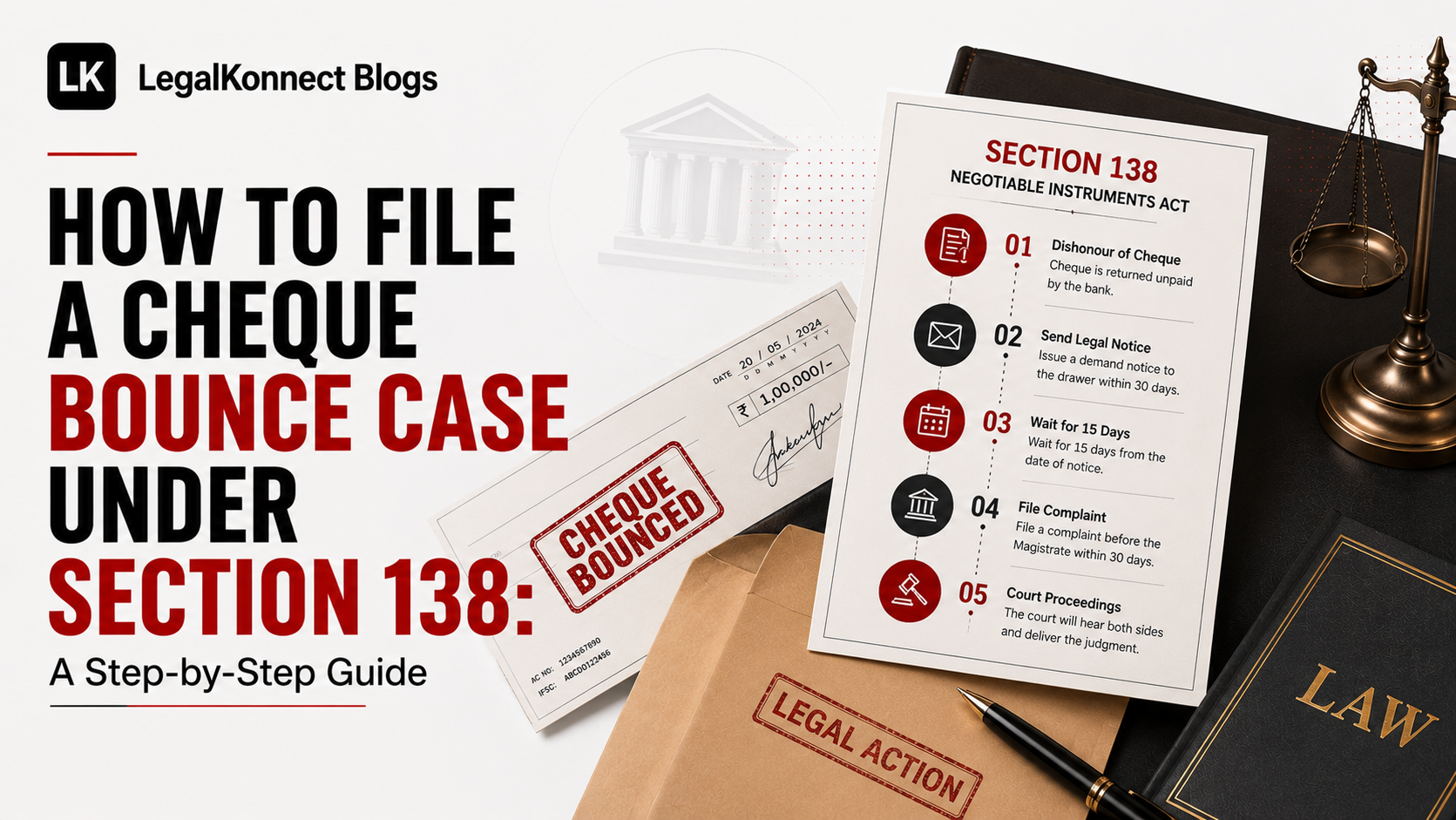

When the cheque bounces, your bank issues a cheque return memo — a slip stating why it was dishonoured. This little piece of paper is the official starting gun for your whole case. The date on it is the date your 30-day notice clock begins.

Keep the original. Don't lose it. Everything downstream — the notice, the complaint, the court's timeline — is calculated from this date.

Step 3: Send the Demand Notice Within 30 Days

This is the step that makes or breaks the case, and it's where most people slip.

You must send the drawer a demand notice — a formal letter demanding payment of the cheque amount — within 30 days of receiving the return memo. No notice, no case. Send it on day 32 and you've lost the right to prosecute on that cheque.

The notice should clearly state: the cheque details (number, amount, date, bank), the fact and date of dishonour, and a demand that the drawer pay the full amount within 15 days. Get an advocate to draft it — a defective notice is a frequent reason these complaints collapse later.

How to send it: registered post with acknowledgment due (RPAD), and keep the postal receipt. Here's a detail people miss — if the drawer dodges the postman and the notice comes back "unclaimed," you're not stuck. In C.C. Alavi Haji v. Palapetty Muhammed (2007) 6 SCC 555, the Supreme Court held that a notice correctly sent to the right address is deemed served even if the drawer avoids collecting it. Avoidance is not a defence.

So what does this mean for you? The defects that sink these cases are rarely about the strength of the debt — they're almost always procedural: a notice sent on day 32, or sent to an address the drawer no longer uses. Send it to the correct address by registered post, fast, and keep every receipt.

Step 4: Wait Out the 15-Day Window

Once the drawer receives your notice, they get 15 days to pay. The clock runs from the date they actually received it, not the date you sent it.

If they pay, good — that's the cleanest possible outcome, and you're done. If they don't, your cause of action (your legal right to file) arises on the 16th day. You cannot file before this. Filing on day 10 is premature and gets thrown out.

This 15-day pause is genuinely useful, by the way. It's the cheapest settlement window you'll ever get — many disputes quietly resolve here, because the drawer now knows criminal proceedings are real.

Step 5: File the Complaint Within 30 Days — In the Right Court

Now the main deadline. From the day your cause of action arises (that 16th day), you have 30 days to file a written criminal complaint before a Magistrate.

And the question that confuses most people: where do you file?

After the 2015 amendment to the NI Act (Section 142(2)), you file in the court where your own bank branch — the branch where you deposited the cheque for collection — is located. Not where the drawer lives. The Supreme Court confirmed this in Bridgestone India Pvt Ltd v. Inderpal Singh (2016) 2 SCC 75. So Meera files in Pune, where she banked the cheque, even though the contractor is in Nagpur.

So what does this mean for you? You litigate on your home ground. That alone removes a huge practical barrier — you're not travelling across the state to attend hearings.

What the Complaint Must Contain

The complaint is filed by you (the payee or holder of the cheque) in writing, and it must include:

The cheque, the return memo, and a copy of your demand notice

Proof you sent the notice (postal receipt, acknowledgment)

A clear statement of the debt and the dishonour

Your evidence on affidavit under Section 145 — the law lets you give your initial evidence in writing rather than orally, which speeds things up

The court takes cognizance (formally decides to proceed) and issues summons to the drawer.

What Happens After You File

The Magistrate issues summons. If the drawer ignores them, a non-bailable warrant can follow. The trial then runs as a summons-trial.

One thing in your favour from the start: Section 139 of the NI Act presumes the cheque was issued against a genuine debt. The burden is on the drawer to prove otherwise. You begin a step ahead — though "a step ahead" is not "guaranteed to win," and a well-advised drawer can rebut that presumption.

A quick currency note, because it trips people up: from 1 July 2024, the CrPC was replaced by the Bharatiya Nagarik Suraksha Sanhita (BNSS), 2023. Your complaint is still filed under Section 138 and Section 142 of the NI Act — that hasn't changed — but the background procedure (summons, warrants, recovery) now runs under the BNSS. If your advocate is quoting CrPC section numbers out of habit, that's the reason for any mismatch.

You Can Get Paid Before the Case Ends: Interim Compensation

You don't have to wait years for the trial to finish before you see any money. Under Section 143A (added in 2018), the trial court can order the drawer to pay you interim compensation of up to 20% of the cheque amount while the case is still going on. On Meera's ₹3,00,000 cheque, that's up to ₹60,000 in her hands during the proceedings.

Be precise about this, because the law is: the statute says the court "may" order it — the Supreme Court has read this as a discretion, not an automatic right. So it's not guaranteed. But it's a request your advocate should make early, and many drawers settle the moment it's granted, because now the case is costing them in real time.

There's a matching pressure point on appeal too: under Section 148, if a convicted drawer appeals, the appellate court can require them to deposit a minimum of 20% of the fine or compensation before the appeal is even heard. The law deliberately tilts the cost of dragging things out onto the person who bounced the cheque.

"I Won — Now How Do I Actually Get Paid?"

This is the question that actually matters, and it's worth thinking about before you file, not after.

A conviction or a compensation order is a piece of paper. It is not money in your account. If the drawer simply doesn't pay, the court's compensation order is recovered the way a fine is recovered — through a warrant for attachment of the drawer's property. In practice, you often have to actively push that enforcement; it doesn't happen on its own.

This is why experienced advocates frequently run a parallel civil recovery suit alongside the Section 138 case. The criminal case creates pressure; the civil suit (or a summary suit) is what actually attaches assets and recovers the sum. Think about recovery on day one — because the judgment is the start of getting paid, not the end.

What It Costs and How Long It Takes

Let's be honest about the price. The demand notice itself is cheap — roughly ₹1,500–5,000 with an advocate. The full case, if it goes to trial, typically runs ₹15,000 to ₹50,000 or more in advocate fees, depending on your city, the cheque amount, and how long it drags. The advocate's time is the real cost, not court fees.

And time is the bigger cost. Cheque bounce cases in India routinely run two to five years, even after the Supreme Court issued directions in In Re: Expeditious Trial of Cases Under Section 138 of the NI Act (2021) to speed them up. Use Section 143A and the settlement windows precisely because the trial itself is slow.

So what does this mean for you? Before you commit, it is worth an honest look at your chances of winning. For a small cheque, send the notice and settle — the threat does most of the work. For a larger amount like Meera's, file, ask for interim compensation early, and run a civil suit alongside it.

Three moves decide most of these cases: send the notice on time, file where your bank is, and claim your 20% early. Get the notice drafted right — book a consultation. Or, if you're the one who received a notice, start here.

Frequently Asked Questions

Common questions about Cheque Bounce

About the Author

Adv. Shivam Mehrotra

Verified advocate on LegalKonnect.

All articles are reviewed for legal accuracy before publication.

Meet the author