Key Highlights

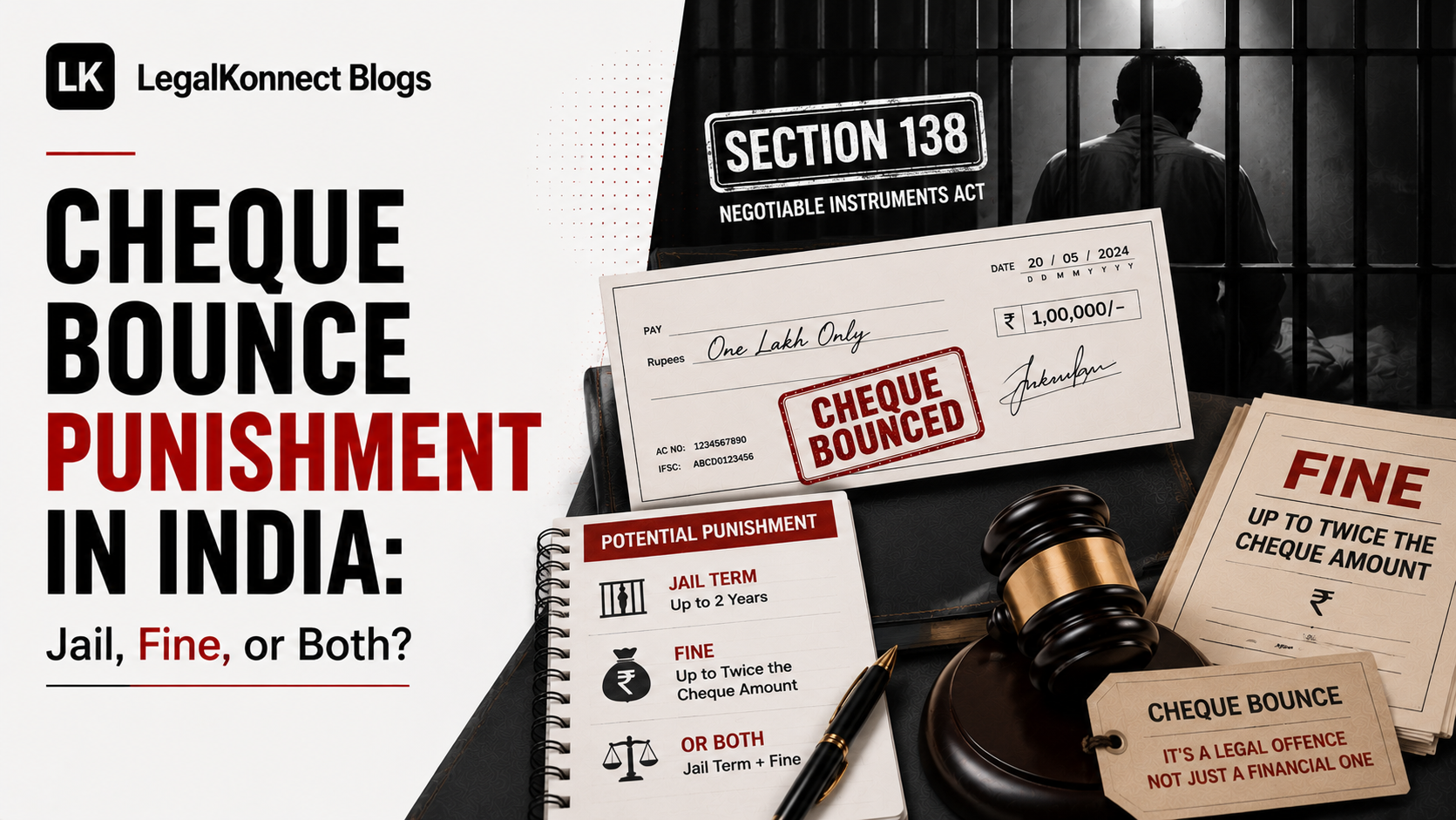

- The maximum cheque bounce punishment under Section 138 is up to 2 years' jail, or a fine up to twice the cheque amount, or both.

- In practice, a first-time bounce almost never ends in jail — it ends in the drawer repaying the money, usually the cheque amount plus costs.

- The offence is non-cognizable, bailable, and compoundable: police can't arrest you off a bounced cheque, and paying up can close the case.

- The "fine" usually goes to the payee as compensation, not to the State — for the victim it's recovery, for the accused it's the real cost.

- Jail mainly happens on default of payment after conviction — and even that is capped at six months for a Section 138 case.

- Company directors and the person who signed the cheque can be personally liable under Section 141.

- Compounding (settling) is allowed at almost any stage — the earlier you do it, the cheaper it is.

The cheque you wrote bounced. A few weeks later a demand notice landed, and there's one line in it keeping you up at night: "punishable with imprisonment which may extend to two years."

Take Rohan, who runs a small auto-parts business in Indore. He paid a supplier ₹4,00,000 by cheque to hold his credit line together. It bounced — "funds insufficient." Now he's reading that two-years line and picturing a cell.

So here's the question Rohan is actually asking, and probably you too: is cheque bounce punishment really jail?

The honest answer, up front: the maximum cheque bounce punishment under Section 138 of the Negotiable Instruments Act, 1881 is two years' jail, a fine up to twice the cheque amount, or both. But a first-time bounce almost never ends in jail — it ends in you paying the money back. Custody mainly hits those who lose and still refuse to pay.

The rest of this explains when jail is real and when it isn't — for the person who wrote the cheque and the person holding it.

What the Law Says About Cheque Bounce Punishment

Section 138 sets the outer limit: imprisonment up to two years, or a fine up to twice the cheque amount, or both. That "or both," and the word "twice," are what scare people. Hold that thought — the maximum on paper and the usual outcome in court are two very different things.

Three features of the offence matter just as much as the sentence:

It is non-cognizable — meaning the police cannot register an FIR or arrest you over a bounced cheque. It is not a police matter. It runs as a private complaint before a Magistrate.

It is bailable — you are not looking at custody on arrest; you'll receive a summons to appear.

It is compoundable — the parties can legally settle it, and we'll come back to why that's your most powerful exit.

The practical upshot: nobody is coming to your door. If a case is filed, the first thing you get is a summons. Not handcuffs. (If you've just received the notice and want the steps, our guide on what to do when you receive a cheque bounce notice walks through the 15-day window.)

But Will You Actually Go to Jail?

Here's the part the two-year line doesn't tell you. The Hon'ble Supreme Court has repeatedly treated a Section 138 case as a recovery mechanism dressed in criminal clothes. In Kaushalya Devi Massand v. Roopkishore Khore (2011) 4 SCC 593, the Court said the offence is "almost in the nature of a civil wrong which has been given criminal overtones," and that its gravity cannot be equated with offences under the penal code.

Translated: courts run these cases to get the payee their money, not to fill jails. For a first-time bounce, where the drawer is willing and able to pay, imprisonment is the exception. Most convictions end in a fine and compensation, not custody.

For Rohan — one bounced cheque, a genuine business reason behind it, and the means to make it good — his realistic exposure is the ₹4 lakh plus interest and costs, not a cell. The question quietly shifts from "will I be jailed?" to "what will this cost me?"

The "Fine" Is Really Your Money Going Back to the Payee

This is the bit that confuses people on both sides. When a court imposes that fine of up to twice the cheque amount, the money does not vanish into a government account. In R. Vijayan v. Baby (2012) 1 SCC 260, the Supreme Court held that the object of these cases is compensatory, and that courts should ordinarily award the complainant compensation — typically the cheque amount, often with simple interest of 9% as the reasonable measure of loss, plus costs.

So that fine isn't the State punishing you. It's mostly your own debt coming back around, with interest. For the payee, that's the prize: recovery, not revenge. For Rohan, it means planning to repay the ₹4 lakh plus 9% interest and costs — and treating that, not a jail term, as the likely bill.

You Can Be Made to Pay 20% Before the Case Even Ends

You don't have to wait years for a verdict for money to start moving. Under Section 143A, added in 2018, the trial court can order the drawer to pay the complainant interim compensation of up to 20% of the cheque amount while the case is still running. On Rohan's ₹4,00,000 cheque, that's up to ₹80,000 — payable during trial.

Be precise here, because the statute says the court "may" order it. In Rakesh Ranjan Shrivastava v. State of Jharkhand (2024), the Hon'ble Supreme Court held that "may" in Section 143A is discretionary, not mandatory — so it isn't automatic. There's a matching pressure point on appeal: under Section 148, if a convicted drawer appeals, the appellate court can require a deposit of at least 20% of the fine or compensation before the appeal is heard.

For a payee, that's worth moving on early — an interim-compensation application often nudges the other side toward a settlement. For Rohan, it means up to ₹80,000 of that ₹4 lakh can be ordered out of his pocket within months of the case starting, long before any verdict.

When a Cheque Bounce Does Lead to Jail

So when is custody real? Mainly in three situations.

First — and most commonly — default of payment. If you're convicted, ordered to pay the fine or compensation, and you simply don't, the court can send you to prison "in default." But this is capped: the imprisonment imposed in default of payment cannot exceed one-fourth of the maximum sentence for the offence. For Section 138, where the maximum is two years, that caps the default term at six months. This cap is the long-settled rule under Section 65 of the old Penal Code, now carried into Section 8 of the Bharatiya Nyaya Sanhita, 2023.

Second, repeat or wilful offenders. Someone with a pattern of bouncing cheques, or who clearly has the means and refuses out of bad faith, is far more likely to draw an actual sentence than a first-timer who's trying to pay.

Third, a currency note that trips people up: since 1 July 2024, the CrPC has been replaced by the Bharatiya Nagarik Suraksha Sanhita (BNSS), 2023. The offence is still under Section 138 of the NI Act — that hasn't changed — but the procedure around sentencing, warrants and recovery of the fine now runs under the BNSS.

So custody here is mostly the price of refusing to pay after losing — not of the bounce itself. If Rohan were to lose and still not pay, his worst case is six months, not the two years printed in the section.

Who Gets Punished When a Company's Cheque Bounces

If the cheque came from a company, punishment doesn't stop at the company. Under Section 141, the company and every person who was in charge of and responsible for the conduct of its business at the time can be prosecuted — which usually pulls in directors and, almost always, whoever signed the cheque.

The rule is settled; whether a particular director is caught turns on their actual role. A director who genuinely ran nothing has been let off; the person who signed the cheque rarely escapes. Courts look at real responsibility, not the title on a visiting card.

The practical point: if you signed a cheque for a company, the liability is personal — the company's name won't shield you.

The Off-Ramp: Paying Can Make the Punishment Disappear

Because the offence is compoundable under Section 147 of the NI Act, you can settle a cheque bounce case at almost any stage — and a genuine settlement ends it. In Damodar S. Prabhu v. Sayed Babalal H. (2010) 5 SCC 663, the Supreme Court laid down guidelines actively encouraging early compounding, and built in graded costs: the longer you wait to compound, the more it can cost you.

In plain terms — pay or settle, file a compounding application, and the court closes the case, usually without a conviction recorded. Do it at the first hearing and it's cheap. Do it after years of fighting and losing, and you pay the money, the escalated costs, and your legal bills.

For Rohan, this is the real exit: pay the supplier, get their agreement, file to compound, and the case closes — usually with nothing on his record. The catch is timing. Compound at the first hearing and it's cheap; do it after years of losing and he pays the money, the escalated costs, and his advocate on top.

The Bottom Line — for Both Sides

If you wrote the cheque, like Rohan, a first bounce you can pay is a money problem, not a jail problem — pay or compound early and you most likely walk away with no conviction. If you're holding the cheque, the punishment is really your leverage; the prize is the money, so push for compensation early.

So before you walk into court, know your exposure. Read our honest take on your chances of winning a cheque bounce case, and if you're the accused, the defence strategies that actually work. Then book a consultation with a verified advocate and get advice on your own facts.

Frequently Asked Questions

Common questions about Cheque Bounce

About the Author

Chandra Mauli Mishra

Verified advocate on LegalKonnect.

All articles are reviewed for legal accuracy before publication.

Meet the author